An unknown research paper

In a research paper, written in 2000, an unknown accounting professor from the University of Chicago developed and successfully tested a ranking system where, with the use of a few simple accounting based ratios he convincingly proved that it can help you make better investment decisions.

Remarkable is that this information seems to be relatively seldom used by investors especially in our local market.

Meet the professor

The developer of the system is Joseph D. Piotroski a relatively unknown accounting professor who shuns publicity and rarely gives interviews.

He graduated from the University of Illinois with a B.S. in accounting in 1989, received an M.B.A. from Indiana University in 1994. Five years later, in 1999, after earning a Ph.D. in accounting from the University of Michigan, he became an associate professor of accounting at the University of Chicago.

The research paper

In 2000, he wrote a research paper called “Value Investing: The use of historical financial statement information to separate winners from losers” (pdf).

He wanted to see if he can develop a ranking system (using a simple nine-point scoring system) that can increase the returns of a strategy of investing in low price to book (referred to in the paper as high book to market) value companies.

What he found

What he found was something that exceeded his most optimistic expectations.

Buying only those companies that scored highest (8 or 9) on his nine-point scale, or F-Score as he called it, over the 20 year period from 1976 to 1996 led to an average outperformance over the market of 13.4%.

This is truly outstanding if you remember that 80% of investment funds do not even beat the index.

Even more impressive were the results of a strategy of investing in the highest F-Score companies (8 or 9) and shorting companies with the lowest F-Score (0 or 1).

Over the same period from 1976 to 1996 (20 years) this strategy led to an average yearly return of 23.0%, substantially outperforming the average S&P 500 index return of 15.83% over the same period.

This average outperformance of the market of just over 7% per year may not seem like much but over the 20 year period an investment of $1,000 in this long short strategy would have grown to $62,820 compared to an amount of only $18,600 if you invested in the S&P 500 index.

The difference between these two rates of return over the 20 year period is over 44 times your initial investment!

Does it also work in Malaysia?

After getting really excited about the returns I asked myself if this would also work in Malaysia and in the current market environment.

But more on that later, lets first look at how the Piotroski F-Score is calculated.

How is the Piotroski F-Score calculated?

The Piotroski F-Score is calculated with the use of the following 9 ratios. For every criteria (below) that is met the company is given one point, if it is not met, then no points are awarded. The points are then added up to determine the best value stocks.

Profitability

- Positive return on assets in the current year (1 point).

- Positive operating cash flow in the current year (1 point).

- Higher return on assets (ROA) in the current period compared to previous year (1 point).

- Cash flow from operations are greater than ROA (1 point)

Leverage, Liquidity and Source of Funds

- Lower ratio of long term debt to in the current period compared value in the previous year (1 point).

- Higher current ratio this year compared to the previous year (1 point).

- No new shares were issued in the last year (1 point).

Operating Efficiency

- A higher gross margin compared to the previous year (1 point).

- A higher asset turnover ratio compared to the previous year (1 point).

If a company has a score of 8 or 9 it is considered strong. If the score adds up to between 0-2 points, the stock is considered weak.

How you can best use the Piotroski F-Score

As you can see from the way the Piotroski F-Score is calculated it is really a measurement of the quality of a company.

The F-Score is thus best used along with another valuation measure such as price to book ratio (as a first screening measure) where after you use the Piotroski F-Score to select only quality companies.

So back to this question……

Does it also work in Malaysia?

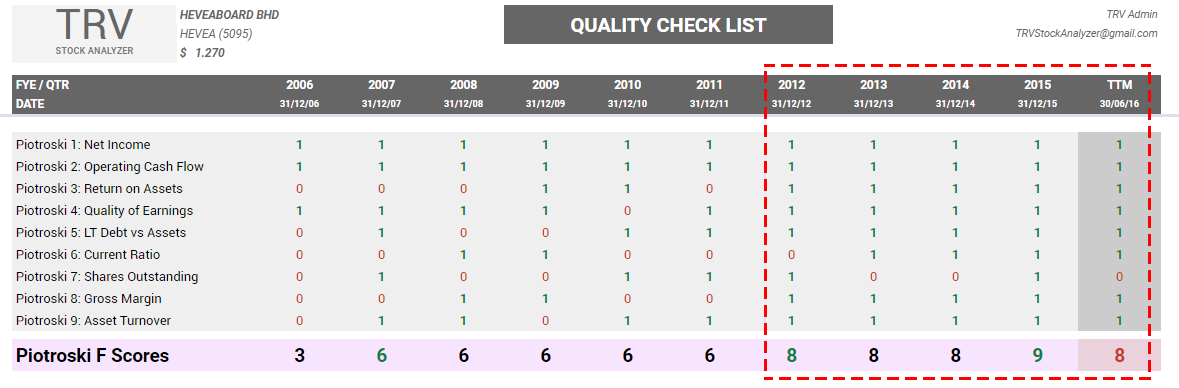

There is lack of research in our local market. But, let us take a look at HEVEA.

Click to enlarge. Diagram showing Piotroski F-Score for HEVEA.

Picture above showing last 10 years Piotroski F-Score for HEVEA calculated using the TRV Stock Analyzer. Highlighted in the red box is year 2012 to 2016 where we can see vast improvement in the Piotroski F-Score. Let us compare to the share price performance.

Click to enlarge. Diagram showing 10 years share price for HEVEA.

Picture above showing last 10 years adjusted price chart for HEVEA. We can see extraordinary gain in it’s share price for the period of 2012 to 2016.

Coincidence?

On my next post, I will be showing more examples of high flyers and their Piotroski F-Score.

Summary

Piotroski F-Score is really a measurement of the quality of a company. It is best used along with other valuation measure.

What is really remarkable is that, in spite of the substantial benefits the F-Score can add, it has not been taken up more widely by investors and the asset management profession.

Leave A Comment